Saving for College vs. Retirement

When budgeting each month, many parents face a trade off between saving for retirement versus saving for your children’s college education. In this trade off, retirement savings may be partially or entirely sacrificed for your children’s future — a valiant decision in the short term that may have serious long-term implications. With this in mind, consider these suggestions before you put all of your eggs into a single basket.

Determine how much of your child’s education you intend to pay for.

In order to do so, research the cost of higher education at the kind of school you hope your child will eventually attend. Look at how much the cost of these schools has increased in the past two decades and create an estimate of how much those schools may cost 10-20 years down the line. With this in mind, you can guestimate how much you need to have saved for college and how much you need to save each month in order to reach this goal. You can also use the U.S. Department of Education’s Net Price Calculator to estimate the cost of attending various colleges. You should also keep your child in the loop throughout the decision process. When they hit high school, your child should already know how much money you plan to contribute to their college education, and they can use this information to plan on how they will pay the difference.

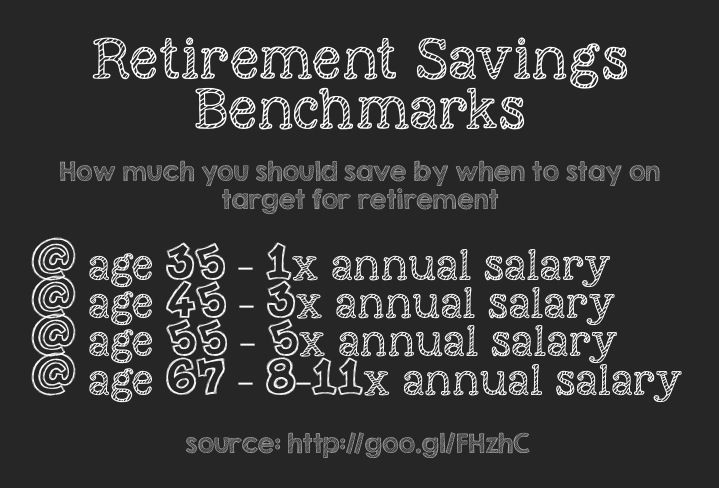

As you budget for your child’s education, do so with retirement savings benchmarks in mind.

See the attached graph for a rough estimate on how much you should have saved during various times of your life. To customize this plan, make an appointment to meet with an ELM3 representative, and we can help you determine how much you should have saved at various points in your life and how much you should be saving each month in order to reach these goals.

It is easier to borrow for college than for retirement.

There are a variety of loans, grants, and scholarships available to students attending college. The same do not exist for retirees. Keep this in mind when determining which savings accounts to prioritize, and make sure your children are researching and applying for all available funding options when the time comes. You should also consider that money in retirement accounts (such as within 401k accounts) is not considered when schools are determining the amount of need-based aid for which your child qualifies. This does not necessarily hold true if you withdraw money from your retirement accounts to pay for higher education; however, the more you set aside for retirement, the more aid your student may qualify for.

Compare interest rates.

Student loan interest rates are often lower than retirement account growth rates. This means that money put into retirement savings accounts will often appreciate more quickly than debt from student loans. While this is not always the case, compare the interest rates of popular student loans and your retirement savings accounts’ growth rates to determine where your money will have the most impact,.

Make a savings priority list.

Such a list will likely prioritize employer-matched 401(k)s, any high-interest debt (especially credit card debt), and emergency funds. After you have contributed to these accounts, you can begin contributing to college savings accounts and other savings vehicles. Of course, your priority list will depend on your specific capacity and needs, and ELM3 would be happy to assist you in building this list.

At the end of the day, it’s important to remember the airplane metaphor: you need to put your own oxygen mask on before assisting others. You’ll be no help to others if you haven’t taken care of yourself first.